Save All Year Long with Discounts from American Family

From going paperless to paying in full, you can qualify for more than one way to save.

Updated April 1, 2024 . AmFam Team

If you're getting money back from the IRS this tax season, you may already have plans on how to spend that employment tax refund. Although it's tempting to start splurging on luxury items or exotic vacations, you could benefit from pausing and asking yourself: what is the smartest way to spend your tax refund?

From making an additional mortgage payment to taking a bite out of credit card debt, that extra bit of cash can go a long way to helping you achieve your long-term financial goals.

The key is to make a list of your biggest fiscal priorities and rank them in order of importance. If you have more pressing needs, like a water heater that will soon need replacement, get that on your list, too. Take a look at these tax refund expense ideas to consider:

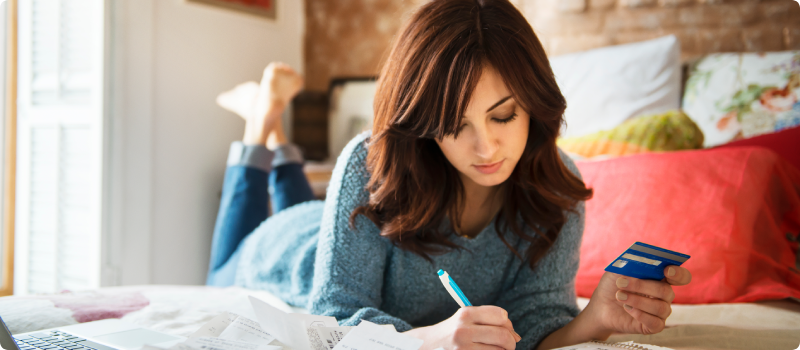

A good way to start your process is to check in with the free annual credit report that Equifax, Experian and TransUnion offer. Carefully review the names of debtors you’re still paying. Rank the debts according to amount.

And be sure to dig into details so you understand your interest rate on each debt. Completely paying off a credit card can greatly improve your credit utilization score, and that can mean good things for your credit report. Consider putting a large percentage of your tax refund toward high-interest debt like:

Paying your kid’s school tuition amount or annual insurance premiums can put more cash into your pocket year-round. It always feels good to take a financial burden off of your plate, and in some cases, you might even qualify for a discount if you pay in full.

Maintenance is important for preventing a costly breakdown in the future. So, if your water heater is aging, or your roof needs replacing, consider spending your tax refund on those updates. Other preventative measures you can take when you have some extra cash on hand might be to replace worn appliances, or taking your vehicle in for a tune-up or new tires.

By picking up smart home technology for your house, you can improve its overall safety and get a heads-up when something’s wrong. You don’t need to do it all at once. Start with a smart home hub that’s compatible with your smartphone. From alarm systems to water and flood sensors, this tech can revolutionize the way you interact with your phone.

Do yourself a big favor and earmark a few dollars this year toward an umbrella insurance policy. With it, you’ll have extra protection that travels with you, wherever you go. It’s an additional layer of coverage — over and above the coverage limits of your existing home or auto policies. You can have more peace of mind if you’re faced with a liability lawsuit with umbrella protection in place.

It pays to invest in yourself. If you have a Roth IRA or a 401k retirement account, this could be the perfect opportunity to bump up or even max out your contributions for the year. According to tax experts, this is a great way to prepare for the future. The younger you are, the more years that compound interest has time to work its magic.

Plan for future medical costs by putting money aside into a checking account for deductibles and maximum out-of-pocket expenses. Take a close look at your healthcare coverage’s terms and conditions to learn about what you’ll be expected to pay.

You can also check in with your insurance company and get details directly from a customer service representative. You may find a greater sense of security during your recovery when you know that you’ve got the money in place for costly dental or medical bills.

Placing a portion of your tax refund into a special emergency savings account will help you manage small problems as they happen. Even a few hundred dollars can really come in handy if you encounter an unexpected expense. More importantly, you’ll save on interest payments because that money can help prevent you from having to use your credit card.

After prioritizing your payout options above, do your best to set aside a small amount of your refund — and do something nice for yourself and your family. Whether it's concert tickets or a spa visit, there's nothing wrong with enjoying a no-guilt splurge once in a while.

Now that you know some practical ways to use your tax refund from Uncle Sam, find out some basics about investing your money to really make the most of your hard-earned cash.

Planning for the future also means taking care of your life insurance needs.

Reach out to your American Family Insurance agent and learn about your life insurance options. You’ll find great protection for everyone that means so much — from an insurance company you can trust.

Life insurance is underwritten by American Family Life Insurance Company.

This article is for informational purposes only and based on information that is widely available. This information does not, and is not intended to, constitute legal or financial advice. You should contact a professional for advice specific to your situation.

This information represents only a brief description of coverages, is not part of your policy, and is not a promise or guarantee of coverage. If there is any conflict between this information and your policy, the provisions of the policy will prevail. Insurance policy terms and conditions may apply. Exclusions may apply to policies, endorsements, or riders. Coverage may vary by state and may be subject to change. Some products are not available in every state. Please read your policy and contact your agent for assistance.